In shock and disbelief, the clerk stared at the screen. Then, he turned to Valmont LeBlanc and began shaking his hand.

The New Brunswicker from Saint-Phillipe and Alfreda Cormier had just won $1 million in the Lotto 6/49.

“A woman behind us in line started crying,” said LeBlanc. “She was excited for us, even though she was a stranger.”

That was in early September.

When they picked up their winnings at the Atlantic Lottery Corporation office in Moncton, the couple said they would use their winnings to cover the cost of renovations, including a new kitchen, and the purchase of a new car to replace their older vehicle. That, and a new truck for LeBlanc.

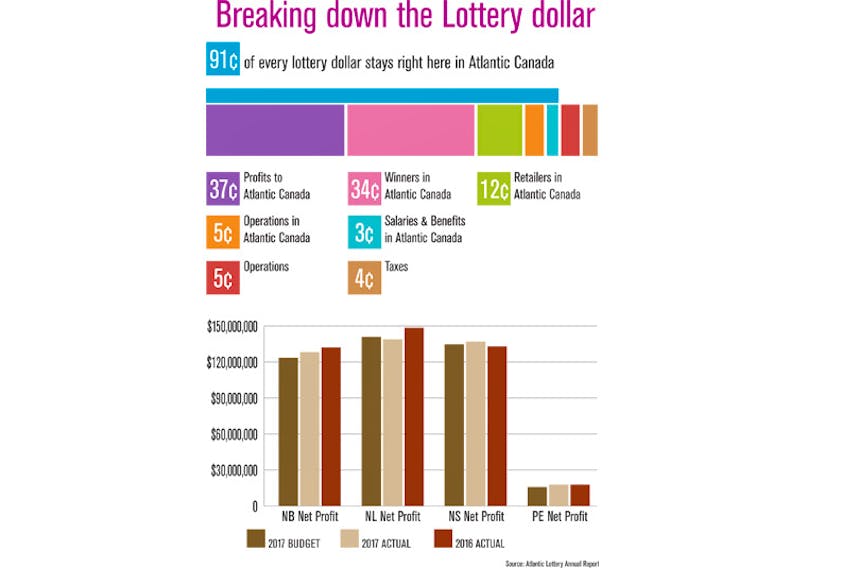

In the past year, Atlantic Lottery Corporation has forked over 16 prizes of $1 million or more in the region, shared by 25 winners. Six of these big payouts went to people in Nova Scotia, five in New Brunswick, one was won in Prince Edward Island, and four in Newfoundland and Labrador.

Two Atlantic Canadians walked away with truly massive, multi-million dollar winnings. In Nova Scotia, Olga Beno took home almost $5.4 million in the Lotto 6/49 and on the Rock Myra Bourgeois raked in more than $4.2 million with her 6/49 ticket.

Many of the winners at first expressed fairly modest plans for that big prize money.

Those down-to-earth plans, though, don’t tell the whole story of what happens to some people who suddenly get a massive windfall.

“A lot of people who win money like this, it’s shocking how many of them wind up throwing it all away in a couple of years and wind up with nothing,” said Blair Corkum, a Charlottetown, Prince Edward Island-based financial adviser.

As bizarre as it might seem to almost everyone who dreams of hitting the jackpot and being financially set for life, there’s also a dark side to big lottery winnings.

“If you’ve not come from this kind of money, then this is like a toxic shock psychologically,” said Dr. Emmanuel Haven, a finance professor and the Dr. Alex Faseruk Chair in Financial Management at Memorial University.

Studies conducted over the past 50 years show that lottery winners are at first overjoyed with their winnings but then tend to settle back down to their previous level of happiness.

Dr. Roy Kaplan’s 1987 paper, Lottery Winners: The Myth and Reality, revealed that American lottery winners more often tended to be older, relatively affluent men. While those who had low-paying jobs did often quit them after striking it rich, those with higher-paying and satisfying occupations just kept on working even after winning the lottery. Most didn’t spend lavishly but rather gave a lot of their winnings to their children and charities.

The most commonly bought things? Houses, cars and trips. Unsurprisingly perhaps, most winners were generally happy with the experience.

The influx of cash from a big jackpot can be a great boon for lottery winners – or the beginning of a downward slide.

That’s what happened to Manitoba resident Gerald Muswagon who won $10 million in 1998. Seven years of partying and a failed business later, Muswagon reportedly hanged himself in his parents’ garage in 2005.

By then, the 42-year-old’s winnings had evaporated.

Cautionary tales of people whose lives fell apart after winning a lottery jackpot are the stuff of urban legend.

Although Atlantic Lottery Corporation doesn’t dole out financial advice, it does give winners five basic tips on which almost all financial experts agree.

1. The first is: wait. Don’t quit your job. Don’t buy tons of things.

“Many of us fantasize about heading to the malls right away, or handing out cheques to family members,” the lottery corporation states on its website. “…. it’s good to spend the first few days taking some time to absorb the news. This means avoiding any large decisions immediately.”

A few days? Think instead of a few months. Get the heck out of town. And avoid social media. It takes time for the reality of that situation to sink in.

“What I would do if I won is probably move out very fast because it’s not just the people you knew from high school (who will come around looking to share in your new wealth) but even people who say, ‘I can invest this for you,’” said Haven.

2. Atlantic Lottery Corporation suggests winners consult with a professional financial adviser.

“Once your money is in the bank, it’s time to consider what to do with it,” states the lottery corporation on its website. “Thinking this through from the outset can make things much easier and straightforward later on. Consult a financial adviser like a bank manager, accountant or investment planner for professional advice based on your personal goals for the future.”

Corkum agrees. He says lottery winners should shop around for financial advice the same way as they would for a new roof to their house.

“You need to talk to probably about three financial advisers to find out what they tell you to do,” he said.

As a fee-only financial adviser, Corkum cannot sell life insurance, annuities or any other investment and make commissions on them. Many other financial advisers, though, do earn commissions on the sale of investment vehicles.

On an exchange-traded fund, which is like a mutual fund but has shares that trade on stock exchanges, a financial adviser will usually get a commission of about a quarter of a percentage point. Segregated funds pay up to about two per cent to the financial adviser in commissions.

3. Unlike in the United States, Canadians who strike it rich in the lottery here do not have to pay taxes on their winnings. But any earnings from those winnings is taxable, even in Canada.

“Contact a tax specialist or Revenue Canada to find out more,” suggests Atlantic Lottery Corporation on its website.

4. Friends, family, financial advisers and would-be entrepreneurs aren’t the only ones who flock to these newly minted millionaires and hold out their hands.

Charities also see an opportunity to get sizable donations. But Atlantic Lottery Corporation cautions its winners to think through a strategy for giving before handing out any money.

5. The only thing financial advisers agree makes sense to do right away – other than sticking the money in a bank and taking some time to let reality sink in – is paying off high-interest credit card balances.

“I would put the money into one of the well-known banks,” said Corkum. “Even if it’s $2 million, the odds of the CIBC or Bank of Montreal going bankrupt is pretty slim.”

Even clearing off a mortgage or car loan, which sound like good ideas, might not be the best moves if this means paying penalties for wiping out those debts early. Corkum advises clients to first find out whether there are penalties for doing that and what those penalties are.

Step one for those who have never had an investment portfolio is to get informed on what types of investment vehicles exist and the risks and benefits that come with them.

“You have to read up on what you want to do with that money so that when you approach that guy at a good, solid Canadian bank, you can at least talk about it,” said Haven.

His own personal strategy would be to open up several bank accounts at different Canadian banks to benefit as much as possible from the up to $100,000 depositor insurance offered by the Canadian Deposit Insurance Corporation. It covers bank accounts and term deposits, including guaranteed investment certificates, with a maturity of no more than five years in Canadian funds.

The finance and economics professor is wary of investing in stocks and advises new millionaires to tread lightly and do their homework.

According to him, a safer bet is to invest a good chunk of the money in mutual funds and bonds as picking the wrong stock can be dangerous.

Boom or bust of winning wealth

Lottery prizes carry with them cautionary tales

STORY CONTINUES BELOW THESE SALTWIRE VIDEOS